France’s taxation regime was a significant cause of revolutionary sentiment. The nation’s taxation burden was carried almost entirely by the Third Estate. As contemporary writing and propaganda suggests, many taxpayers felt overburdened and frustrated by this lack of equality. This article outlines how France’s tax regime operated, who paid tax, how it was collected and the problems this created.

Excessive, inefficient, unfair

Taxation was a significant problem in late 18th-century France. According to conventional wisdom, the Ancien Régime’s taxation regime was excessive, inefficient and unfair.

It was excessive because France had become one of the highest-taxing states in Europe, chiefly because of its warmongering, its growing bureaucracy and high spending. It was inefficient because many taxes were collected by a network of private contractors dubbed ‘tax farmers’, a system that encouraged graft, corruption and tax avoidance.

It was unfair because the bulk of the nation’s direct taxation was levied on the Third Estate. France’s common people, who could least afford to pay, believed they were shouldering most of the nation’s tax burden while the privileged First and Second Estates paid little or nothing, despite their comparatively greater wealth.

Unsurprisingly, grievances about the Ancien Régime’s unbalanced and inequitable taxation regime became a significant cause of the French Revolution. But were these grievances valid?

Origins of the taxation crisis

France’s issues with taxation date back to the reign of Louis XIV (1643-1715). National expenditure increased markedly during the reign of the ‘Sun King’, driven by military spending, participation in several wars, the expansion of the state bureaucracy and extravagant spending on Versailles and the royal court.

Funding for these policies was left to Jean-Baptise Colbert, Louis XIV’s innovative comptroller-general [treasurer] in the mid-1600s. Colbert sought to strengthen the national treasury by increasing revenue and curtailing unnecessary spending.

To achieve this, Colbert reclaimed lands, abolished thousands of pointless royal offices, implemented mercantilist policies to generate income from France’s colonies, encouraged the growth of domestic production and passed laws to regulate domestic trade. These reforms were effective and government revenues grew rapidly during his ministry.

These increases did not match the king’s increased spending, however, and by the 1670s France was again in fiscal trouble. Colbert returned to the desperate revenue measures he had previously abandoned, such as selling royal lands and venal offices, acquiring loans from foreign bankers and raising new taxes.

‘Tax farmers’

Colbert also tried increasing tax revenue by improving systems of collection. Most tax revenues were collected by hundreds of private ‘tax farmers’ (state-contracted debt collectors). In 1680, Colbert created the Ferme Générale (‘General Farm’), an attempt to streamline tax collection by reducing the number of tax farmers.

When Colbert died in 1683, the government was receiving almost 93.5 million livres in net revenue – more than triple the 32 million livres it was receiving when he became controller-general in 1661.

After Colbert’s death, however, control of the national finances passed to less capable men. By 1715, annual tax receipts had plummeted to less than 31 million livres. This revenue shortfall would plague the nation for the rest of the 18th century.

Forms of taxation

There were two categories of tax in pre-revolutionary France: direct taxes and indirect taxes. Direct taxes were levied on individuals and collected by royal officials. Indirect taxes took the form of duties and excises on goods and were collected by ‘tax farmers’.

By the 1780s, indirect taxes made up almost half the government’s taxation revenue while direct taxes accounted for about one-third. In addition to royal taxes, some members of the Third Estate made obligatory payments to their lord and the Catholic church. Peasants living in a seigneurie, for example, paid a cens (land royalty) and champart (a share of the harvest) to their lord.

France’s peasants were also subject to the corvée, an obligation to provide unpaid labour on infrastructure such as roads. Many peasants also paid a tithe or dime: a share of the harvest given to the Catholic church. While not formally state taxes, these obligations were often considered part of the taxation regime.

Direct taxes

The taille was the oldest of France’s state taxes. It was also the royal government‘s most lucrative impost, bringing in about 20 million livres a year. The taille was first levied in the 15th century to meet the costs of the Hundred Years’ War. It was intended as a payment for military service, so the Second Estate (who fought) and the First Estate (who could not fight) were exempted from payment.

The taille was calculated according to the value of property owned and income received. This was done arbitrarily, however, and the amount could vary significantly from year to year. The taille was also easy to evade, particularly for city dwellers, which meant the burden fell mostly on peasants and rural landholders. This inconsistency made the taille the most unpopular of all royal taxes. A pamphlet published in 1694 said of this direct tax:

“The great evil of the taille is the unequal manner in which people are assessed by the authorities and the collectors, who favour their own friends to the detriment of the rest. Industry is taxed, so are talent, exertion and success. Every improvement a farmer makes on his ground exposes him to a heavier taille. A poor cobbler or other artisan, who has nothing in the world but his labour, is assessed four or five crowns a year. A baker at Gonesse, near Paris, who has not an inch of land, is assessed for his personal estate 1,200 French crowns.”

The capitation was a poll tax or ‘head tax’ levied on every adult citizen. It was first introduced in 1695 as a wartime measure. At first, the capitation was levied progressively, each individual paying an amount determined by their profession. There were 22 different payments levels, ranging from one livre to 2,000 livres. The clergy was exempted from the capitation. Members of the nobility were not exempt, though over time they found ways to greatly reduce the amount paid.

French citizens in the 18th century were also subject to income taxes. Like the capitation, these taxes were raised to offset the costs of France’s imperial wars. The first of these income taxes was the dixième, levied by Louis XIV in 1710 at the rate of one-tenth of annual income. It was replaced by the vingtième (one-twentieth of annual income) in 1749. The vingtième was renewed at the beginning of the Seven Years’ War in 1756 and again in 1760. Most expected the tax to be withdrawn when this war ended in 1763 but Louis XVI’s cash-strapped ministers continued to renew it, despite opposition from the parlements and constant grumbling from the people.

Indirect taxes

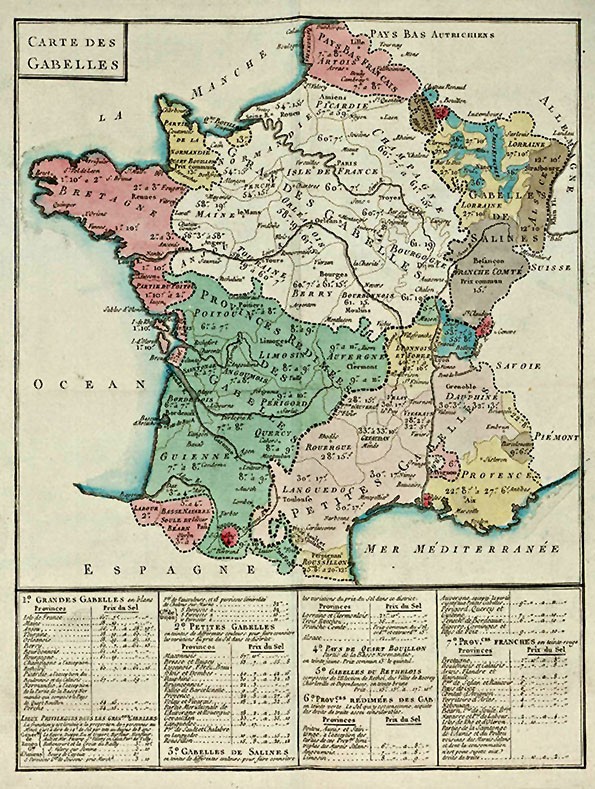

The gabelle was a duty payable on salt. Used chiefly as a food preservative and also in manufacturing and industry, salt was an essential commodity in 18th century France. The gabelle applied to all purchases of salt, whether for private or commercial use. To prevent smuggling, black-marketeering and avoidance of the gabelle, salt was sold in minimum amounts at official stores.

The gabelle was unevenly applied, however, and varied wildly from place to place. The amount of gabelle payable in and around Paris could be as much as ten sous (half a livre) per pound, while provinces in France’s south and east paid much smaller amounts or were entirely exempted. By the 1780s, the gabelle raised more than 55 million livres per annum, or more than 10 percent of the royal government’s taxation revenue. The gabelle was widely unpopular because it was payable by everyone, including peasants. It was also very difficult to avoid.

The importing or trade of food, drink and consumer goods was also taxed indirectly, in the form of excises, customs duties and tariffs. Wine, the most popular alcoholic drink in 18th century France, was subject to a heavy excise called the aide. A similar excise called tabac applied to the sale of tobacco. The traites were a series of customs duties, payable by merchants importing goods from abroad or from one province to another. The octroi was a municipal tariff on goods entering large cities, particularly Paris.

These duties and excises affected merchants, traders and businessmen more than individuals. Indirect taxes were so important that many French cities maintained their high medieval walls, forcing goods coming into the city to pass through the gates where they were inspected and taxed.

Abuse and corruption

“The Farmers-General purchased the privilege of collecting taxes and paying state debts for the various government departments. Taxes thus passed through private hands, and some of it wound up in private pockets. There was no central bank to provide economic stability, only a group of businessmen who sought to find the best balance between a functioning government and their own profits… Given exceptional powers to collect the money, tax-farmers bore arms, conducted searches and imprisoned uncooperative citizens. The money collected over and above that specified in the contract with the government went to the tax farm.”

James Maxwell Anderson, historian

Most indirect taxes were gathered by 40 fermiers-généraux or ‘tax-farmers’: wealthy individuals who acquired the right to collect taxes on behalf of the government. This was such a profitable enterprise that each fermier-généraux paid the royal government up to 80 million livres for a six-year lease. In good economic times, when production and trading were up, some tax-farmers made several million livres per year.

This privatised and unregulated method of tax collection was naturally open to abuse and corruption. The collection methods used by the fermiers-généraux and their agents could be arbitrary, heavy-handed and sometimes brutal.

By the reign of Louis XVI, the fermiers-généraux had become one of the wealthiest groups in France. They purchased grand homes along Paris’ Place Vendôme, venal offices and noble titles. What they could not buy was respect. The fermiers-généraux was one of the most hated institutions in 18th century France, cursed for their ruthlessness and condemned for their greed. Many attributed the nation’s financial woes not to the king or his ministers but to the avarice and corruption of the fermiers-généraux and their employees.

Did taxes significantly increase?

According to folklore, French revolutionary ideas were embraced by a Third Estate that felt overburdened and crushed by a hefty tax burden. This perspective is found in contemporary visual propaganda, which depicts commoners carrying the weight of the nobility and clergy.

Based on this, it is reasonable to believe French taxes were increased significantly through the 1700s – but this was not the case. Taxes rose in some areas (Paris most notably) and fell in others. Overall levels of taxation increased in the half-century preceding the revolution but on its own, this increase was not large enough to incite revolution on its own.

As Gail Bossenga puts it: “the real problem with French taxation seems not to have been its crushing weight but its inequities, inefficiencies and imperviousness to true reform”. In the public mind, taxation with no regard for equality, efficiency or accountability was just as intolerable as being grossly overtaxed.

1. Taxation is considered an important cause of the French Revolution. The accepted view is during the 1700s, France’s taxation regime became excessive, inefficient and unfair.

2. The French were subject to a range of direct taxes (payable to the royal government) and indirect taxes (payable on items like salt, wine and tobacco) as well as feudal payments.

3. Direct taxes were collected by royal officials, while indirect taxes were collected by the fermiers-généraux or ‘tax-farmers’, an unpopular group accused of rampant greed and corruption.

4. Tax liabilities varied widely across France. The gabelle or salt tax, for example, was levied at much higher amounts in Paris and surrounding provinces than in southern France. The nobility and clergy were also exempt from some direct taxes.

5. A commonly-held view in the 1780s was that the Third Estate was being overtaxed and forced to carry the tax burden of the First and Second Estate. While the reality was more complex, it was clear the taxation regime was in dire need of reform.

Citation information

Title: ‘Taxation as a cause of revolution’

Authors: Jennifer Llewellyn, Steve Thompson

Publisher: Alpha History

URL: https://alphahistory.com/frenchrevolution/taxation/

Date published: September 11, 2019

Date updated: November 7, 2023

Date accessed: April 26, 2024

Copyright: The content on this page is © Alpha History. It may not be republished without our express permission. For more information on usage, please refer to our Terms of Use.